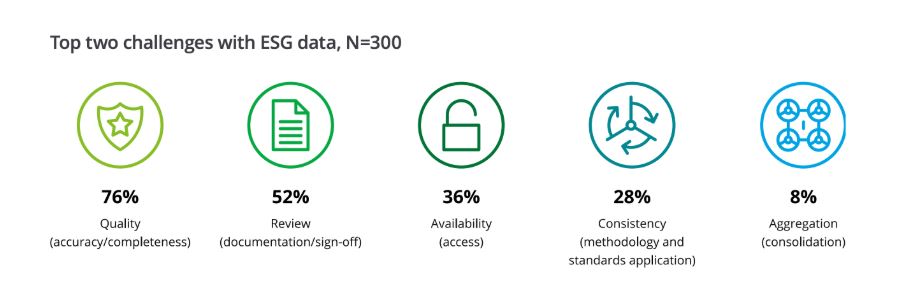

For most enterprises, ESG data accuracy now sits at the top of the reporting agenda. In Deloitte’s survey of 300 senior executives, 57% identified data quality as their company’s primary ESG data challenge, ahead of all other concerns.

The reasons are structural. Sustainability reporting has shifted from voluntary, unassured disclosure to mandatory, audit-ready filings — governed by CSRD in Europe, ISSB-aligned regimes across Asia-Pacific, and California’s SB 253 in the United States. ESG figures are now subject to the same controls, lineage, and third-party assurance once reserved for financial reporting, and the consequences of weak data have moved from reputational to regulatory, financial, and litigable.

This guide examines what is driving that shift, where ESG data accuracy most often breaks down, and how specialized ESG data research services can help. Let’s begin!

Why ESG Data Accuracy Is Now a Material Risk

- Regulatory and Compliance Risk: As ESG disclosure requirements expand across jurisdictions, companies need traceable data, defined controls, and audit-ready reporting processes. Fragmented or poorly documented ESG data increases the risk of disclosure gaps, restatements, enforcement actions, and financial penalties.

- Reputational Damage and Greenwashing: Sustainability claims around emissions, net-zero targets, supplier practices, or social impact must be backed by defensible evidence. When those claims cannot be substantiated, companies face greenwashing allegations from regulators, investors, advocacy groups, and the public, which can damage trust beyond the original disclosure.

- Capital Access and Financing Costs: Investors, lenders, and rating agencies increasingly use ESG data to set pricing, allocate capital, and structure sustainability-linked financing. When that data is incomplete or fails external assurance, companies face covenant triggers in sustainability-linked loans, financing-cost step-ups, restated disclosures, and reduced eligibility for ESG-screened indices and funds.

- Divergence Across ESG Ratings: ESG ratings vary because providers use different scoring models, weightings, and materiality assumptions. Without clear and consistent source data, companies have limited ability to explain rating differences or challenge unfavorable assessments, which can influence investor perception, index inclusion, and sustainability-linked financing.

- Inadequate ESG Risk Management: Poor ESG visibility limits a company’s ability to identify and prioritize risks across operations and supply chains. Climate exposure, energy volatility, labor practices, human rights concerns, and supplier non-compliance may remain unaddressed until they create operational disruption, financial loss, or compliance failure.

The Structural Shift Behind These Risks

Sustainability reporting is shifting from voluntary, unassured disclosure to mandatory, audit-ready filings. The same internal controls, data lineage, and third-party assurance that once applied to financial figures now apply to ESG numbers.

The regulatory map itself is fragmented. The EU operates the Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD). Asia-Pacific markets are rolling out ISSB-aligned regimes. In the United States, California’s SB 253 fills the gap left by stalled federal rulemaking. The frameworks differ, but the underlying discipline they impose is consistent: ESG numbers must be defensible to the same standard as financial ones.

Core Challenges Across ESG Data Accuracy

Environmental Data: Fragmented Sources and Variance

Environmental data — emissions, energy use, water consumption, waste, and biodiversity impact — is generated across multiple operations, facilities, and supply chain tiers, with no single system of record. The figures are typically built from low-response supplier surveys, spend-based estimates used in place of activity-based data, and manual transcription of energy bills into spreadsheets. Each step introduces variance that compounds through downstream calculations, undermining the accuracy of headline metrics.

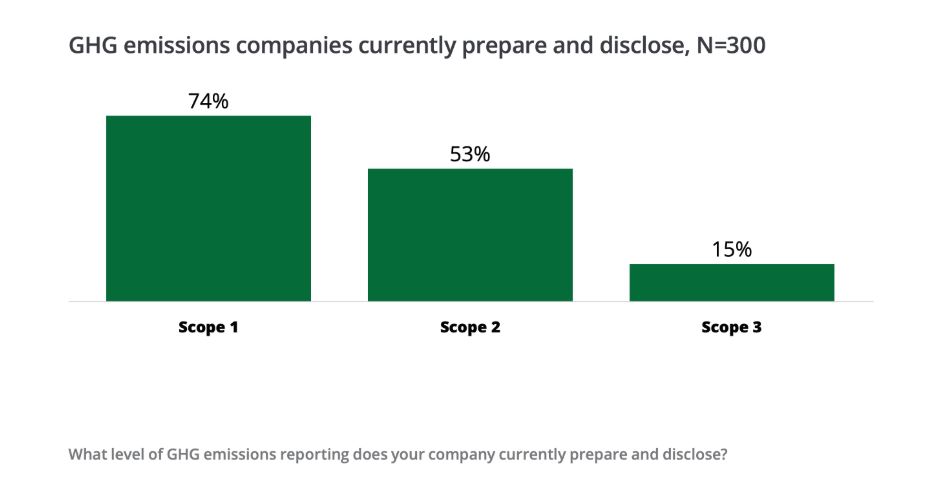

Scope 3 emissions illustrate the scale of the problem. They account for roughly 75% of total corporate emissions, yet remain the least disclosed category by a wide margin.

Social Data: Unstandardized Inputs and Reconciliation Gaps

Social data covers workforce composition, diversity, pay equity, health and safety, human rights, and labor practices across employees and suppliers. Five issues compound to undermine accuracy:

- Subjective Indicators with No Shared Benchmark: Labor practices, employee well-being, and community impact are inherently qualitative. Companies measure them inconsistently across regions, and no numerical standard anchors the comparison the way the GHG Protocol does for emissions.

- Fragmentation Across Internal Systems: Social data is held in HR, payroll, health and safety, and procurement systems in incompatible formats. Producing a single consolidated disclosure typically requires manual reconciliation across each of these systems.

- Heavy Reliance on Self-Reporting: Most social data is self-reported by the company or its suppliers, with little independent observation. This dependency creates room for selective disclosure and social washing.

- Limited Supply-Chain Visibility: Direct suppliers may be auditable, but tier-two and tier-three subcontractors typically are not. Labor and human-rights indicators deeper in the value chain remain largely invisible to the reporting company.

- Data Privacy Constraints: Privacy laws across jurisdictions — including US state statutes and General Data Protection Regulation (GDPR) — restrict how granularly employee demographics, compensation, and health data can be collected. These constraints often limit what can be disclosed even when the underlying data exists.

When these issues stack up, social disclosures fail under scrutiny. Investors, auditors, and procurement teams find numbers they cannot trace, verify, or compare against peers — which is when the data accuracy gap becomes a commercial and reputational liability.

Governance Data: Inconsistent Taxonomy and Data Lineage

Governance data covers board composition, executive compensation alignment, audit committee independence, ethics policies, lobbying activity, and cybersecurity oversight. Many of these indicators are qualitative by nature and difficult to benchmark or standardize across companies and regions.

The data also sits across legal, HR, compliance, and investor relations functions, with no shared taxonomy between them. According to KPMG, 47% of organizations still use spreadsheets to aggregate their data rather than integrated systems. This introduces human error and breaks the audit trail back to the source.

Even when governance disclosures fall within the scope of ESG assurance, the qualitative nature of many indicators makes them harder to verify than the quantitative environmental data sitting alongside them. The result is the same indicator drifting between filings, weak lineage back to source, and disclosures that companies cannot fully substantiate when regulators or investors examine how a figure was produced.

Best Practices for ESG Data Accuracy

Establish Governance and Internal Controls

Assign clear responsibility for each ESG metric to specific roles across HR, operations, finance, procurement, and sustainability. Apply the same rigor to ESG data as to financial data through internal controls over sustainability reporting (ICSR). Build in ESG data validation checks, segregation of duties, and periodic gap analyses to identify unreliable sources before external reporting.

Adopt a Primary Disclosure Framework

Select ISSB (IFRS S1 and S2) or ESRS as the primary framework, based on regulatory exposure. Map secondary disclosures under GRI against the primary framework. This maintains consistent definitions across filings and avoids parallel reporting structures.

Implement Integrated ESG Data Management Systems

Replace spreadsheet-based workflows with ESG-specific software or ERP modules. Connect these systems directly to utility meters, ERP platforms, Human Resources Information Systems (HRIS), and procurement databases. Direct integration reduces transcription error and removes the need for manual re-entry between source systems and disclosure reports.

Leverage Technology and Automation for Data Capture and Validation

Replace fragmented spreadsheet workflows with specialized ESG software or cloud-based ERP systems that serve as a centralized source of record. Connect systems directly to utility providers, HRIS, ERP platforms, and supply chain databases. This minimizes manual entry and reduces human error.

Configure automated validation rules for anomaly detection, variance thresholds, and missing‑data checks. Run these rules as data enters the workflow. Avoid manual review steps before disclosure. Pair automation with human‑in‑the‑loop oversight. Domain experts review flagged anomalies and validate edge cases. They apply judgment to context‑sensitive disclosures.

Maintain Data Lineage and Consistent Measurement

Ensure every disclosed figure is traceable to its source through a documented data lineage. Keep units of measurement consistent across reporting periods, including metric tons of CO₂e for emissions. Document restatements in line with the same standards applied to financial restatements.

Obtain Third-Party Assurance

External assurance provides independent verification of disclosed ESG figures, reducing exposure to greenwashing claims. Limited assurance is the standard under CSRD and most current regimes. Reasonable assurance signals stronger internal controls to investors, lenders, and rating agencies, even where regulators do not yet require it.

ESG Data Operations: A Strategic Decision for the Enterprise

Most in‑house teams face high fixed costs for hiring, training, and licensing compliance software. These costs rise as regulatory standards like CSRD, ISSB, and the EU Taxonomy evolve.

Outsourcing ESG data research replaces fixed costs with variable, project‑based delivery. Enterprises gain access to analysts skilled in current ESG frameworks. They also benefit from AI‑driven tools for ESG data collection and validation. Outsourcing enables faster ramp‑up on complex reporting cycles.

For CSRD assurance, ISSB transitions, and California SB 253 timelines, outsourcing provides critical support. Internal teams can focus on strategy and disclosure governance. Specialists handle ESG data work required for audit‑ready disclosures.