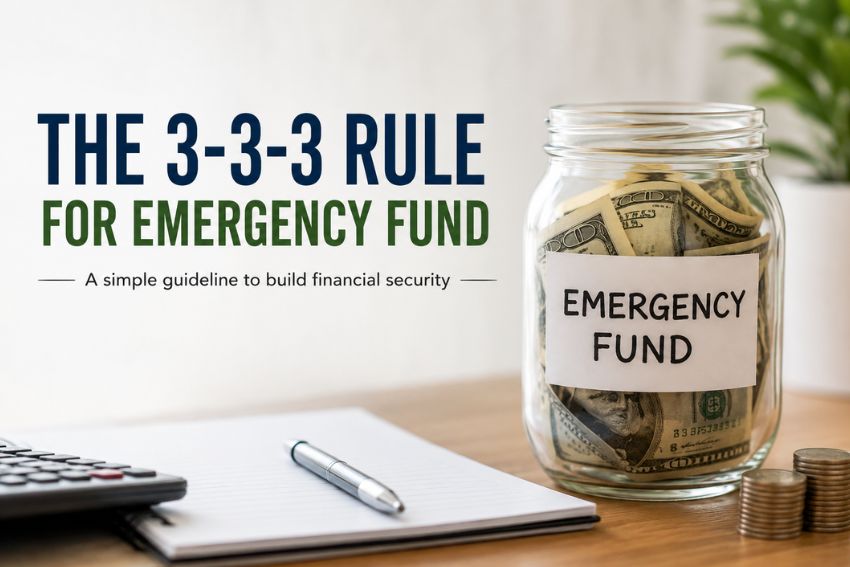

The 3-3-3 rule for emergency fund is a straightforward, no-nonsense strategy designed to ensure your hard-earned cash is accessible exactly when you need it most. Instead of throwing all your savings into one account and hoping for the best, this rule breaks your emergency stash into three distinct buckets. Each bucket serves a specific purpose, balancing the need for instant liquidity with the desire to earn a little something on the side.

Chartered Accountant Nitin Kaushik popularized this approach, and it’s quickly gaining traction as a practical alternative to the traditional “three to six months of expenses” advice. The core idea is simple: an emergency fund isn’t about chasing high returns. It’s about having a financial shield that works instantly when life throws you a curveball.

Breaking Down the 3-3-3 Rule

So, how does this rule actually work? The name gives you a big hint. It involves dividing your emergency fund into three parts of ₹30,000 each, totaling ₹90,000. While the ₹90,000 figure is a suggested starting point, the real genius lies in the structure of the three buckets.

Here is the breakdown of each bucket:

Bucket 1: The Immediate Access Fund (₹30,000)

This is your first line of defense. You park this money in a high-interest savings account, preferably with a bank that offers a competitive rate—think around 6-7%. This bucket is for emergencies that can’t wait a single second. We’re talking about sudden car repairs, an unexpected medical bill, or a last-minute flight for a family emergency. The money is right there, accessible via your debit card or a quick transfer.

Bucket 2: The Slightly Better Return Fund (₹30,000)

The second bucket goes into a sweep-in fixed deposit. This is a smart middle ground. Your money earns a bit more interest than a standard savings account, but it’s not locked away. The key feature is that it “breaks” automatically when you need the funds. This means you get better returns without sacrificing accessibility.

Bucket 3: The Secondary Backup Fund (₹30,000)

The final piece of the puzzle is a liquid mutual fund. This acts as your secondary backup. While it might take a day or two to access, it offers a slightly higher return potential than the other two buckets. It’s your safety net for larger, less time-sensitive emergencies, ensuring your primary buckets don’t get completely drained.

Why This Structure Works

The beauty of the 3-3-3 rule is its focus on liquidity over yield. Many people make the mistake of locking their emergency savings into investments with higher returns, only to face penalties or delays when they need the cash most.

Think of it this way: you wouldn’t lock your fire extinguisher in a safe to keep it shiny, would you? Kaushik uses this exact analogy, noting that an emergency fund is your safety net, not a side hustle to maximize gains. Emergencies don’t come with a T+2 notice; they demand action, instantly. This rule ensures you have a tiered response system for any financial shock.

Is the 3-3-3 Rule Right for You?

The 3-3-3 rule for emergency fund is an excellent starting point, especially if you’re new to building a financial safety net. It provides a clear, actionable framework that removes the guesswork from saving. However, it’s important to tailor it to your personal situation.

Your total emergency fund should ideally cover three to six months of essential living expenses. For some, ₹90,000 might be more than enough. For others, particularly those with high monthly expenses or dependents, it might be a starting goal. You can easily scale this rule up. Instead of ₹30,000 in each bucket, you could aim for three months of expenses in each.

How to Get Started Today

Building your emergency fund doesn’t have to be overwhelming. Here is a simple action plan to put the 3-3-3 rule into practice:

- Calculate Your Baseline: Figure out your monthly essential expenses. This includes rent or mortgage, utilities, groceries, and debt payments.

- Set Your Target: Multiply that number by three. This is your minimum target for each bucket. If your monthly expenses are $1,000, your target for each bucket is $3,000, totaling $9,000.

- Open the Right Accounts: Research and open a high-yield savings account. Look into sweep-in fixed deposit options with your current bank. Finally, find a reputable liquid mutual fund.

- Automate Your Savings: Set up automatic transfers from your checking account to these three buckets each month. This makes saving effortless.

- Protect Your Fund: Ensure you have adequate health insurance. A major medical expense can wipe out your entire emergency fund in one go. Proper insurance acts as a crucial backup to your backup.

The Final Word

The 3-3-3 rule for emergency fund is a powerful, practical strategy for anyone looking to build financial resilience. It cuts through the complexity of personal finance and offers a simple, actionable plan. By prioritizing quick access to cash and peace of mind over chasing market gains, you’re not just saving money—you’re buying security. Don’t wait for a crisis to realize the importance of this. Build your safety net today, and remember, when it comes to your emergency fund, boring is exactly how it’s supposed to be.